May 31, 2024

Slower-than-expected GDP growth in Q1 is more ammo for a June rate cut, economists say

The Bank of Canada adopted the role of the Grinch this holiday season by delivering a final 50-bps rate increase at its last meeting of the year.

It was the Bank’s seventh consecutive rate increase and brings the total cumulative rate increases over the year to 400 bps.

The announcement was mixed news for mortgage borrowers.

On the one hand, this latest hike continued to increase the borrowing costs for those with variable mortgage rates. On the other, the Bank finally indicated that a follow-up rate hike in January is not a given, and that it will instead monitor economic data over the next month and a half to see whether rates need to rise anymore.

“Looking ahead, Governing Council will be considering whether the policy interest rate needs to rise further to bring supply and demand back into balance and return inflation to target,” the Bank said in its statement.

Reaching the end of this rate-hike cycle

It was a message that was repeated by Deputy Governor Sharon Kozicki the following day when she said any further moves by the Bank would be data-dependent.

“If we are surprised on the upside, we are still prepared to be forceful. But we recognize that we have raised interest rates rapidly and that their effects are working their way through the economy,” she said. “In other words, we are moving from how much to raise interest rates to whether to raise interest rates.”

In its rate announcement, the Bank indicated it will be watching inflation, economic growth and jobs figures closely between now and its next rate decision on January 25, 2023.

Last week’s “relatively aggressive hike suggests that the Bank remains acutely concerned about still-high inflation expectations, even amid a clear cooling in domestic demand and some early indications that underlying inflation is losing momentum,” noted BMO chief economist Douglas Porter.

“In recognition of those latter factors, the Bank has opened the door to the possibility that this could be the last rate hike of the cycle,” he added.

A rise in borrowing costs

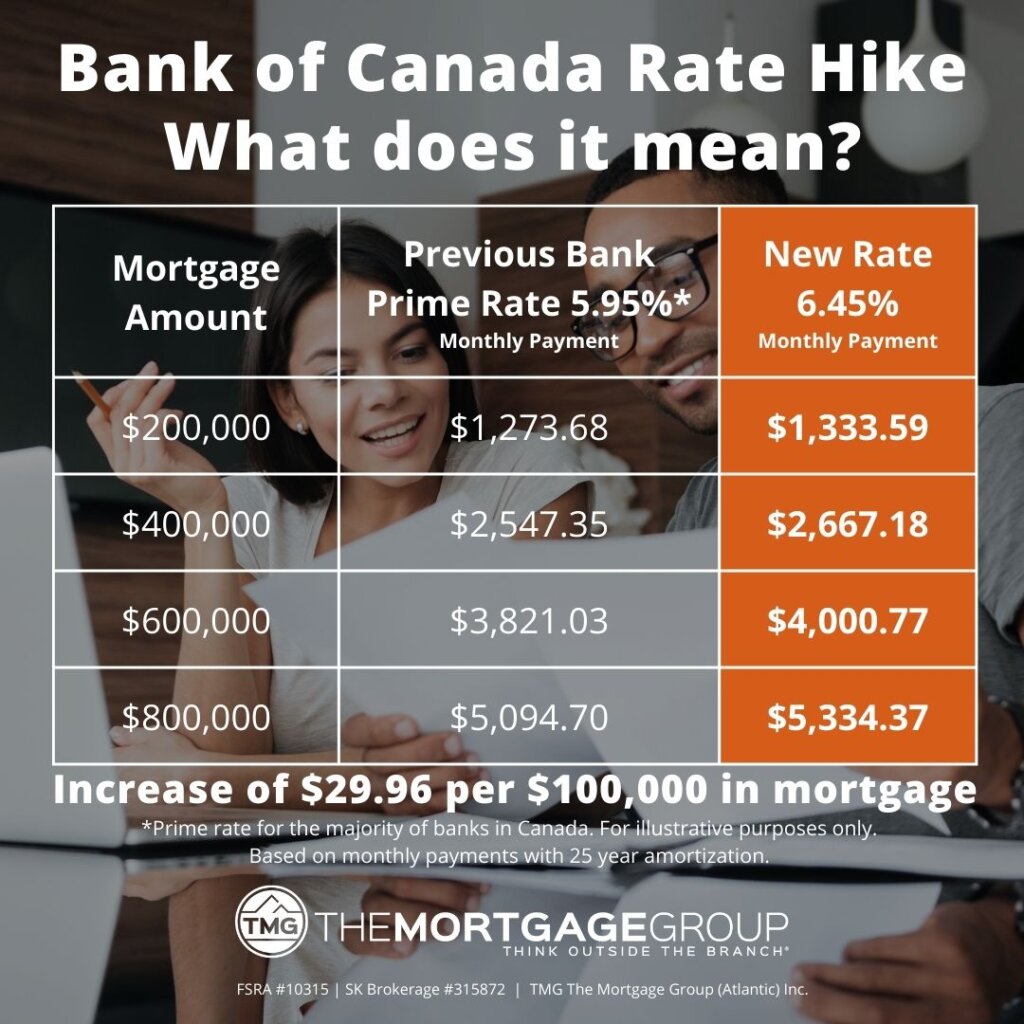

The latest rate hike ratcheted up borrowing costs for mortgage holders for the seventh time this year.

The 400-bps of cumulative rate hikes this year have increased monthly payments for variable-rate mortgages by a little over $200—or approximately 50%—per $100,000 of mortgage based on a 25-year amortization.

Prime rate, upon which variable-rate mortgages and personal and home equity lines of credit are priced, ends the year at 6.45% for most mortgage lenders.

The table below illustrates some sample increases that variable-rate borrowers will face on their upcoming mortgage payments as a result of the latest increase to the prime rate.

Variable rates are now on average about half a percentage point higher than comparable fixed rates. The increase will continue to have an impact on affordability, further blunting any benefits prospective homebuyers might have seen from easing home prices.

When might rates start to fall?

But looking ahead, near-zero growth in the Canadian economy by the middle of the year is expected to lead to falling interest rates by the end of next year or early 2024.

“We can now see a marked slowing in real estate entailing an extremely rapid deflation in that market,” economists from National Bank wrote in a research note. “To calm inflation, in our view, it will not be necessary to keep interest rates high for long and we accordingly expect the central bank to ease substantially in the second half of next year.”

All of this can be a lot for anxious borrowers to digest, especially those with mortgages coming up for renewal or those in the market to purchase.

A big question is whether expectations of falling rates in the next year are reason enough to continue to explore a variable or other short-term rates.

That’s a decision that a mortgage broker can help you make based on your personal circumstances and risk tolerance.

But TMG mortgage broker Dave Larock of Integrated Mortgage Planners thinks those with the “stomach for it” may benefit from an overall lower borrowing cost by taking a 5-year variable mortgage vs. a 5-year fixed, even if variable rates are comparatively higher today.

“I think there is still a reasonable chance that 5-year variable rates may prove to be cheaper than their 5-year fixed-rate equivalents over their full term because of future rate drops,” Larock wrote in a blog post.

“While I fully expect the BoC to overtighten and to wait longer than the consensus expects to cut its policy rate once inflation is finally brought to heel, I expect the BoC to lower its rate rapidly when we finally do reach that point,” he added.

“Simply put, if you’re willing to pay more over the first half of your term, I think there is still a decent chance that you will recover that excess cost, and then some, over the second half of your term.”

For those concerned about rising monthly payments, a mortgage broker can go over your options, whether you’re looking to purchase, renew or refinance.